Most people are scared of the word budget. It’s often seen as a dirty word in many households because people feel like a budget will just suck the fun out of everything. A budget doesn’t have to remove the fun from your life, but failing to plan for fun in your budget will!

I love a zero-based budget because you can plan for exactly what you want and not have to sacrifice the fun stuff.

This blog post will outline all the positives (and a few negatives) of using a zero-based budget as well as go through an example of exactly how it works. You ready? Let’s do this.

Table of Contents

What is a Zero-Based Budget?

A Zero-Based Budget is an easy to use budgeting method where your income – expenses = zero. Sounds simple, right? That’s because it is. When working with a Zero-Based Budget you take the time each month to plan where every single penny of your income will go. This can sound super daunting at first, but don’t worry it’s not that complicated.

This budget just plans where you’ll spend your income before you get your hands on it. The benefit of planning before you have the income is that you’re less likely to make impulse decisions if you already have a plan!

How Does a Zero-Based Budget Work?

The first step to a successful Zero-Based Budget is to estimate your total income for the month. This includes income from your employment, any government cheques that may come, child support, etc. If you live on an irregular income, you can take an average income for the past few months and see how far you can get.

The next step is to figure out what expenses you’ll be working with. There are a few categories of expenses that you can have.

Your needs:

- Housing (Mortgage/Rent)

- Utilities

- Groceries

- Child Care

Your wants:

- Eating Out

- Pocket Money

- Cell Phone Bill

- Gift Giving

Transportation:

- Car Payment

- Gas

- Insurance

- Bus Pass

- Taxi/Uber/Lyft

Saving/Debt/Investing:

- Emergency Fund

- Student Loans

- Credit Cards

- House Downpayment

- Investments

- Retirement

So, at the beginning of each month, you’ll have to list all of your expenses for the month and assign them a certain percentage of your income. Remember, no two months are the same so chances are you’re going to have to adjust every time you create a budget. One month you may have a cash increase and you’ll be able to save more, the next month you may have 5 birthdays to deal with. Always adjust your budget!

If you create your budget and your expenses are higher than your income, you have two choices:

- Increase Your Income

- Decrease Your Expenses

Benefits of a Zero-Based Budget

A Zero-Based Budget gives you complete control over where your money goes. You can change the categories at any time when your circumstances chance and add things in when you need to have a little fun. You can add a travel fund and go on a trip, it’s all up to you.

This system eliminates any impulse purchases because every single penny has a value and a place where it goes, so you can’t just spend $15 on ice cream and chocolate if it’s not in the budget. This budget really allows you to prioritize your expenses and not your wants, which will get you closer to your goals.

Example of a Zero-Based Budget

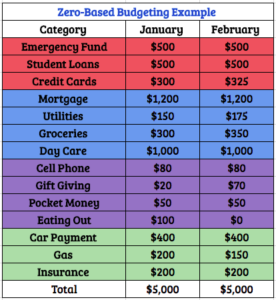

There is no better way to understand something than to actually see it in action, so that’s what we’re going to do. I’ve created this two month zero-based budget example for a single mother who makes $5,000 each month (after taxes). She has two children and wants a better future for them so she decided to start using a zero-based budget so she doesn’t have to worry about her money as often as she used to.

She’s a typical person, she has student loan debt, credit card debt, and a mortgage. She wants to make sure she’s safe if something bad happens, so she puts $500 in an emergency fund each month.

As you can see, there are small changes to the budget from month to month. One month she had to go out for a birthday dinner so she had a $100 eating out budget, and the next month was $0. She decided to start carpooling a few days a month so her gas expense went down. She has more birthdays in February so she had to increase her gift giving expense!

As you can see, no matter what changes are made each month the total amount is always $5,000 which is equal to how much money she brings in each month!

Is the Zero-Based Budget right for you?

Chances are this type of budget will have you experiencing some growing pains, especially in the beginning. It’s hard to start a budget when you aren’t used to thinking about your money. It’s super important to start thinking about it, so you can build your future. This budget could be the key to getting you out of a paycheck to paycheck lifestyle. It will help you build a future where you’re able to organize everything and be a better spender!

If you don’t like how organized this budgeting system is, you can also try out the 50/30/20 Budgeting Method which gives you a little more of a loose system!

Final Thoughts

If you have any questions about how to get this process going for you, be sure to ask them in the comment section below and I’ll be sure to help you out!

Thanks so much for reading, be sure to share this post on Pinterest so your friends can see it too!

xo Taylor

Share it on Pinterest!

Thanks Taylor. Great article, easy to understand and to implement. I will try it immediately, and let us hope it will help me put things in order.

Thanks for reading!! I hope it helps

This was a good read! It is an interesting way to set up a budget.

Thanks for sharing! I am excited to try it out!

I hope it works for you!